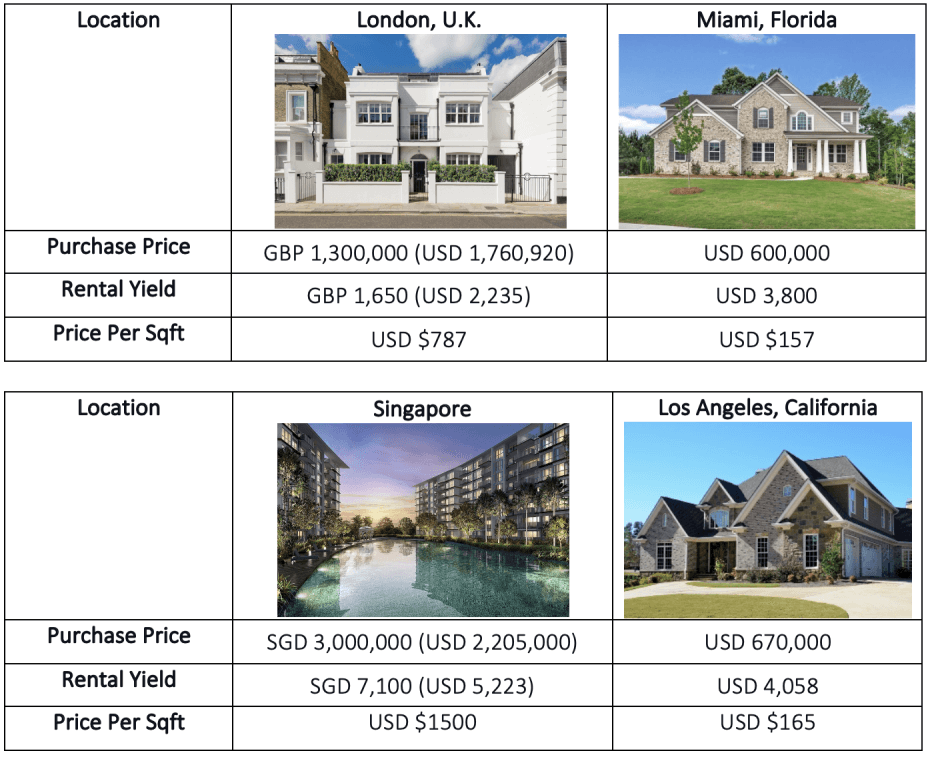

Everyone wants to live in The Bu…

The Bu is, of course, Malibu, California… known as the mecca for Airbnb rentals as well as Charlie Sheen’s house in ‘Two and a Half Men.’

One thing the pandemic has done for all of us is force us to think about the next stages of our lives – family, kid’s education, retirement, all intertwined into where you vacation. We have seen unprecedented demand for vacation home financing over the past 12 months. This is an area where many banks will not lend given the lumpy rental income, normally from renting out on Airbnb or VRBO – but that has all changed!

A report by Redfin shows that demand for vacation homes– otherwise known as short-term rentals –is soaring at a record pace. With an active real estate market, rates hovering around historic lows, and with AM Holiday/Airbnb Investor Program, this moment is the ideal opportunity, whether you are a U.S. expat or foreign national, to consider investing in a vacation home.

Introducing AM Holiday/Airbnb Investor Program

Qualify for a U.S. mortgage loan for a U.S. property that will be used for short-term rental such as Airbnb by using only the projected rental income of the property. No longer are you having to spend hours, days, or weeks collecting tax documents, pay statements, translations, etc. AM Holiday/Airbnb Investor Program allows you to get up to 75% LTV in all 50 states. The best thing, you can get pre-approved for this loan within 72 hours, and once approved, you’ll be issued an “approval letter,” which will allow you to go shopping! It’s as easy as it sounds.

There are a few benefits to possessing a holiday investment property. As of late, Airbnb and VRBO continue to grow as an ever-increasing number of properties are being listed. The convenience of such apps has made it that much easier for homeowners to find and market vacation rentals. In turn, the number of people interested in vacation rental investments has skyrocketed. Purchasing a vacation home can be particularly engaging and ideal when you toss in these personal and financial advantages. Here are some of the benefits of investing in a vacation rental:

1. Tap into rental income

Being a second homeowner presents the chance of leasing it out when you’re away. What’s more, assuming your second home is a great property in a desirable town, transforming it into an investment property will provide you with a subsequent source of passive income. Even celebrities like Leonardo DiCaprio, Jennifer Lawrence, and 50 Cent lease their vacation properties. How cool is that? In some cases, you can even offset the costs of leasing your vacation home. You may even be able to use your vacation home to generate rental income when you aren’t there. This could turn the home into a serious passive income producer in popular tourist destinations.

2. Build home equity.

In conjunction with your vacation home being a fun place to relax, it is also a long-term investment that could flourish your wealth and diversify your portfolio. Build equity on your home as your make mortgage payments. The real estate market and home values often vary. Consequently, the choice to buy a vacation home shouldn’t be made with the assumption that the property’s value will give a colossal result later on. However, your house being located in a highly sought-after town might improve the probability of your property increasing in value over time.

Not only can you generate rental income by leasing out your property, but you also have the benefit of vacationing there yourself; now that’s pretty awesome!

3. Tax Write-offs

Investors should take advantage of the tax benefits related to vacation rentals. Your holiday home is considered a business if it is leased for at least 2 weeks per year. This is very helpful for tax purposes because although the rental’s pay will be taxed, you will be able to write off several of the vacation property’s expenses. You can deduct numerous items from your taxes, including utility expenses, costs of maintenance and repairs, property management fees, mortgage interest, and more. (please consult with your tax advisor)

4. Simplify your vacation!

Bid farewell to hotels. Your holiday home makes it simple for loved ones to gather in one place without stressing over the cost of accommodation. Regardless of whether your home is close to the beach, on a lake, or in the country, there’s a possibility this property will turn into your family’s go-to vacation for any season. By owning a vacation home, you get to decide how long you want your travel to be and who will join. What’s better is that you get to save what you would have spent on hotel or rental accommodations somewhere else!

5. Retirement preparation

A holiday home could ultimately become a full-time home. Purchasing a vacation property when you’re young could provide you with an ideal place to retire in the future. You’ll be able to pay off your home mortgage before it even turns into your main residence. After you retire, the profit from your first home can go toward the current mortgage of your vacation home.

This will successively make your retirement progress simpler, considering that you’re now acquainted with the area, community, and most of all, the home.

Regardless, putting resources into vacation rentals can be a reliable asset for the future.

Should you purchase a vacation home?

If you’re still not convinced, here are 3 other reasons why we think you should snap up this trendy opportunity:

- Mortgage rates are still at record lows

- Vacation homes are in trend; everyone is getting in!

- Short-term rental opportunities with vacation homes

A 2019 study of in excess of 7,000 get-away mortgage holders who recorded their property at a vacation rental site VRBO uncovered that around 40% utilized the rental profit as a secondary income.

What is the ideal location for a summer home?

As an investor, you’d expect quick returns from your get-away rental investment; you’ll need to purchase property in an ideal area to purchase a vacation rental – a popular tourist destination. This could mean beaches, amusement parks, lakes, national parks, or even stadiums. All things considered, it’s not generally the popular destinations that attract tourists. Work travel is another significant opportunity—with a regular clientele.

Here’s a list of the top vacation home areas around the U.S., together with its median monthly rental income:

1. Whittier, North Carolina

Median home sale price: $178,000

Median Monthly Rental Revenue: $3,133

2. Killington, Vermont

Median home sale price: $208,828

Median Monthly Rental Revenue: $3,444

3. Myrtle Beach, South Carolina

Median home sale price: $213,950

Median Monthly Rental Revenue: $2,674

4. Sevierville, Tennessee

Median home sale price: $239,976

Median Monthly Rental Revenue: $5,647

5. Davenport, Florida

Median home sale price: $255,390

Median Monthly Rental Revenue: $2,904

6. Kissimmee, Florida

Median home sale price: $264,863

Median Monthly Rental Revenue: $3,436

7. Gulf Shores, Alabama

Median home sale price: $345,135

Median Monthly Rental Revenue: $4,206

8. Fort Bragg, California

Median home sale price: $509,500

Median Monthly Rental Revenue: $4,508

9. Palm Springs, California

Median home sale price: $ 539,370

Median Monthly Rental Revenue: $6,054

10. Waikoloa, Hawaii

Median home sale price: $575,422

Median Monthly Rental Revenue $4,360

11. Big Sky, Montana

Median home sale price: $585,000

Median Monthly Rental Revenue $6,358

Is Owning A Vacation Rental A Good Investment?

With AM Holiday/Airbnb Investor Program, we say yes! The advantage of purchasing a holiday home is that you get to spend a greater amount of your time rejuvenating. Rather than stressing about paying for a stay at a hotel each time you visit, you’ll bask in the comfort of your own abode.

Vacation properties vary from traditional rentals in that the income a vacation home generates is often subject to the season. A beach house will draw in more interest in the summer, while a place close to a ski resort will thrive in winter.

That being said, though, a vacation rental property is still an excellent method to get passive income.

The tax benefits, passive income, and the option to travel to your very own vacation home are only a portion of the benefits that investing in a rental property can bring you.

Speak to us to find out all about AM Holiday/Airbnb Investor Program specifically for U.S. expats and foreign nationals at [email protected].

www.americamortgages.com